- What is PCI DSS? Is it a Law or a Regulation?

- What are Some PCI DSS Levels?

- The Ecosystem of PCI DSS Regulation Compliance

- Critical PCI DSS Compliance Requirements

- Importance of PCI DSS Compliances

- Challenges of PCI DSS Compliances

-

How to Effectively Implement PCI DSS Standards? Best Practices to the Rescue

- Target to Minimize the Scope of Compliance

- Define SAQs (Self Assessment Questionnaires)

- Organize a Critical Gap Analysis

- Take Advantage of Tokenization and Encryption

- Organize Regular Monitoring and Testing of Systems

- Train Employees to Keep them Aware of PCI DSS Compliance

- Adopt a Proactive Approach to Remain Compliant

- Mistakes to Avoid While Implementing PCI DSS Standards

- Latest in PCI DSS Standards: v4.0 & 4.0.1

- Wrapping Up

Did you know In 2024, data breaches caused a financial loss of $4.88 million? Such numbers aren’t only eye-popping; these are a wake-up call for any business handling sensitive data. When it comes to sensitivity, there’s rarely anything out there that beats financial info.

When security breaches are nothing less than the new normal, PCI DSS standards and protocols alike are the shields protecting people’s card data.

Payment Card Industry Data Security Standard (PCI DSS) is for any size of company involved in storing financial information such as debit or credit card details. Additionally, any parties involved in executing transactions, including merchants, payment processors, service providers, and gateways, are responsible for complying with PCI DSS guidelines.

What is PCI DSS? Is it a Law or a Regulation?

The short answer is None of that! PCI DSS is neither a law nor a regulation. Instead, it’s a framework. As a framework monitored by some financial giants, it provides a safer ecosystem by shaping standards that revolutionize the safety of monetary transactions.

The PCI DSS standards are designed and maintained by the Payment Card Industry Security Standards Council (PCI SSC). The council members include Visa, MasterCard, American Express, Discover, and JCB, among others.

These council members are handling the majority of transactions worldwide. As a result, they are using this dominance to get their payment partners to sign contracts for a safer financial system.

What are Some PCI DSS Levels?

Four levels fall under the PCI DSS compliance regulations. Whether you are a fintech owner or a merchant, these levels don’t exist just for tick boxes. Instead, each level helps tailor security requirements based on the merchant’s ability to handle transactions.

For anybody, including the owner of a retail store or an MNC, PCI DSS levels ensure everybody involved in the transaction can protect users’ payment data.

| Level | Criteria | Requirements | Who It’s For |

|---|---|---|---|

| Level 1 | Over 6 million transactions annually (all channels) or identified as high-risk |

| Large-scale businesses, e-commerce giants, global retailers |

| Level 2 | 1 million to 6 million transactions annually |

| Medium-sized businesses, regional retailers |

| Level 3 | 20,000 to 1 million e-commerce transactions annually |

| Small to mid-sized e-commerce businesses |

| Level 4 | Fewer than 20,000 e-commerce transactions annually OR up to 1 million total transactions (all channels) |

| Small businesses, local shops, and service providers |

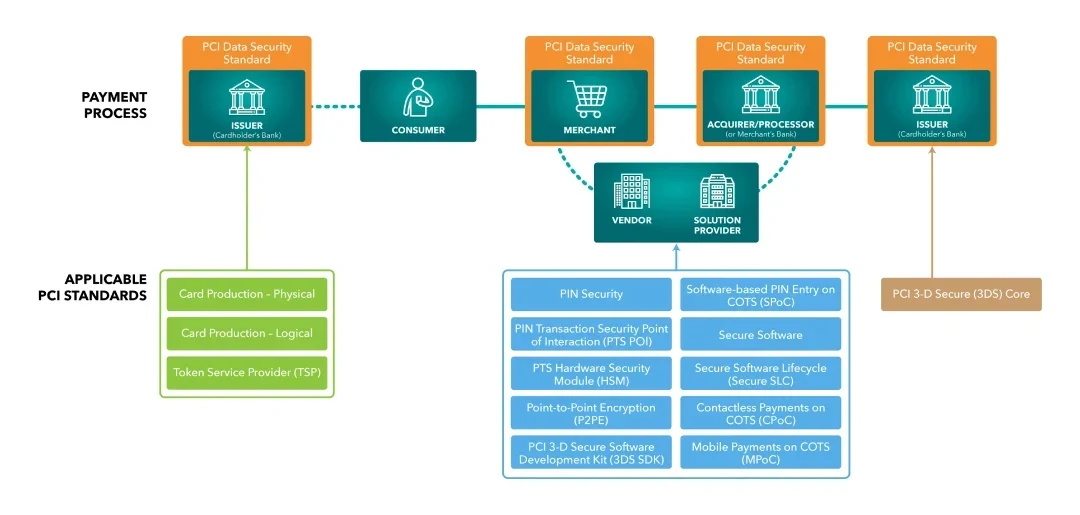

The Ecosystem of PCI DSS Regulation Compliance

The PCI Security Standards Ecosystem, as defined by the PCI SSC focuses on each stakeholder of the process. To better understand, the best way is to dive deeper. Let’s begin!

The Key Players in the Payment Ecosystem

Key players in the implementation of the PCI DSS standards ecosystem refer to the entities that are supposed to participate in these regulations. These entities are:

- Issuers: These are the banks and NBFCs that issue debit and credit cards. Such authorities keep an active eye on transactions and approvals. In parallel, they establish measures against financial crimes, such as fraud detection tactics.

- Merchants: Any business that accepts payments through cards has to follow PCI DSS guidelines for the safety and security of their customer’s financial information.

- Acquires/Processors: These are the service providers or financial institutions that ensure the smooth flow of transactions between the sender and the receiver.

- Vendors and Solution Providers: These are experts focused on fintech products. They’re supposed to take care of PCI DSS IT requirements to ensure that the fintech apps or software they build are safe.

Layers of PCI DSS Standards

PCI DSS compliance requirements are multilayered. To understand them well, you have to dissect each layer. Here’s our overview that can help:

- Card Protection: The layer is designed to cover cards from their physical production to logical elements like tokenization. Tokenization is strongly recommended by PCI DSS for its ability to replace actual card details to counter cyberthefts.

- Encryption Technologies: PCI DSS compliance regulations apply standards like Point-to-Point Encryption (P2PE) to safeguard the data during its transfer. This makes it hard for unauthorized parties to steal information by making it unreadable.

- Software-Based PIN Entry: This sets up a secured payment gateway that exists on commercial off-the-shelf (COTS) devices like smartphones, tablets, etc. The goal of this gateway is to make payments more flexible while keeping them safe.

- Mobile and Contactless Payments: The rise of mobile payment gateways is enabling features like contactless transactions, tap-to-pay solutions, etc. PCI DSS ensures payments remain secure.

Advanced Security Features

PCI DSS's purpose goes beyond implementing basic financial security measures. It takes some extra measures that enable enhanced security protocols centered around almost every transaction, major or micro. Here are some additional measures covered by PCI DSS in fintech.

- PIN Transaction Security: PCI DSS has protocols in place to protect the security of PINs. These measures include checking incorrect PIN entries in point-of-sale (POS) systems, regularizing ATM audits, and checking attempts like data tempering.

- Safer Fintech Software Development: Relevant authorities set some ground rules for PCI DSS in fintech development companies. They are supposed to use frameworks like PCI 3-D Secure (3DS) to enhance fraud detection and prevention tactics. This helps them ensure a safer outcome whether they’re building a mobile banking app or software.

- Token Service Providers (TSPs): PCI DSS emphasizes tokenization for its ability to hide financial data such as card details. For cyber attackers with the intention of stealing financial information, it gets hard to identify actual details.

Consumer

Everything comes together for this one goal- securing the data of the consumer making transactions. PCI security compliances perform as a shield to ensure this. From offering security protocols for each layer to tokenization of financial cards, all activities are designed to reduce financial risks and possible fraud.

As a part of these consumer-centric tactics, fintech companies are also organizing campaigns to make customers more aware of their obligations related to financial security. These campaigns are done through social media platforms, text messaging, emails, newsletters, etc.

Critical PCI DSS Compliance Requirements

PCI DSS standards have several requirements defined in its handbook to avoid possible cyberattacks. Here’s a quick summary:

Building and Maintaining a Secure Network

- Requirement 1: Installing and maintaining a firewall configuration to enhance the security of the cardholder data.

- Requirement 2: Recommends elimination of vendor-supplied defaults for system passwords and security systems.

Secured Cardholder Data Storage

- Requirement 3: The requirement ensures cardholder data is well encrypted and tokenized to reduce the risk of leaking original payment details.

- Requirement 4: This clause of the PCI DSS certification requires encrypting the information in transit. This is done by using advanced cryptographic protocols centered around secure communications.

Implementation of a Vulnerability Management Program

- Requirement 5: The requirement instructs keeping systems safe against malware and updating antivirus software regularly.

- Requirement 6: This guides fintech companies to release configurations and patches regularly to ensure no application-level flaws remain.

Restricting Access to Cardholder Data

- Requirement 7: It restricts the cardholder data to people in positions where cardholder data is crucial to use. This is called Role-based Access Control (RBAC).

- Requirement 8: This places a procedure for creating unique IDs, strong passwords, and multi-factor authentication.

- Requirement 9: Ensures the physical access to the cardholder data is restricted and ensures the physical environment and devices keeping financial data are well protected.

Monitoring and Testing Systems

- Requirements 10: It empowers devices to comply with PCI DSS compliance regulations to tackle system errors or configuration weaknesses. Requirement 10 mandates keeping a log of system activities.

- Requirement 11: It mandates penetration testing to identify possible vulnerabilities in the system. The goal of the requirement is to keep an eye out for unauthorized wireless access points.

Maintain an Information Security System

- Requirement 12: The requirement asks financial institutions to maintain a policy that ensures addressing the security of information for all personnel involved in any transaction.

Importance of PCI DSS Compliances

PCI DSS checklist in fintech plays a critical role beyond implementing an ecosystem of regulations. Its importance enhances security, transparency, and trustworthiness. PCI DSS compliance process just doesn’t keep systems running; it keeps them invincible. Here’s a detailed outline of how PCI DSS standards help:

Preventing Data Breaches and Fraud

One of the main pain points of fintech companies is continuous attempts of data breaching. PCI DSS gives such businesses a handbook of rules, allowing them to strengthen their security posture.

In 2019, a major data breach in the USA at the First Amercian Financial Corporation was detected. It exposed that between 2008 and 2024, there were over 885 million financial records of the people.

Keeping the Brand Reputation Safe

An ISACA Study announced in 2022 that data breaches compelled 1 out of every three customers to cut ties with the victim brand. Implementing Payment Card Industry Standards reduces the possibility of data breaches, helping brands keep their reputation intact.

Enabling Secured Innovation

As tech trends evolve, fintech solutions evolve in parallel. This evolution is powered by configuration settings and patches. By setting up some standards, PCI DSS ensures these patches are properly configured to maintain the security and integrity of digital products.

Supporting a Global Payment Ecosystem

PCI DSS standards set up a global transaction system that speeds up transactions and settlements while keeping security prioritized. Combined with technologies like Smart Contracts, payment card data security standards make it possible to move money faster while keeping secured records logged and free from the threats of possible cyberthefts.

Additional Benefits of Implementing PCI DSS Requirements

PCI DSS helps businesses expand across the boundaries of their countries by making transactions safer and more collaborative. In a digitally secured environment, these transactions can also get settled faster, improving the overall user experience as a result.

For a deeper insight, these are some benefits your PCI DSS checklist can unlock.

Standardization of Security Practices

Aligning with PCI DSS requirements can be great for making your fintech company or financial product align with global standards. This can result in faster approvals and a financial environment that is much safer, trustworthy, and more collaborative.

Enhanced Customer Trust

PCI DSS sets a trust factor in the mind of the user whenever they come to your product. This trust factor is what multiplies your product’s reputation making it more popular. Especially for customers who are very conscious about the security of their financial information, the implementation of payment card data security standards can be a major trust factor.

Competitive Advantage

Complying with PCI DSS guidelines can give your business a competitive edge over companies that are still operating traditionally. You can show off the PCI DSS certification across your payment platforms to impress your customers.

Avoiding Penalties

PCI DSS violations can lead to penalties that can range up to $5,000 to $100,000 per month. By having proper enforcement of these guidelines you save yourself from an additional layer of expenses.

Challenges of PCI DSS Compliances

PCI DSS standards are useful but also paired with certain challenges, especially for businesses that have just started their journey. These challenges can be:

Complex Requirements

PCI security compliances include 12 main requirements with over 300 individual controls. For businesses, it can be hard to implement and interpret all of them in parallel, requiring them to invest in additional expert resources.

Evolving Standards

PCI DSS standards are continuously evolving in parallel with cyber threats. Transitioning from PCI DSS 3.2.1 to 4.0 is a recent example of this evolution. This enforces a requirement for businesses to comply with evolving requirements, ultimately costing them additional money.

Resource Constraints

Payment card industry standards require resources. New businesses and bootstrapped startups might find it difficult to allocate dedicated resources to keep up with what these standards require and how often they change.

Third-party Risk Mitigation

Very often, businesses involve third parties in transactions, which adds another layer of complexity. Ensuring these third parties remain compliant with PCI DSS regulations can be a task that requires additional resources.

Employee Awareness and Training

Organizing sessions to keep all employees informed and trained for PCI DSS compliances can be difficult for companies. Such a process requires PCI DSS training for each new hire and regular sessions to ensure all employees have coverage. Even after all that, it is critical to ensure employees are maintaining PCI DSS requirements in their projects, if applicable.

How to Effectively Implement PCI DSS Standards? Best Practices to the Rescue

PCI DSS compliance application across your business can feel like an overwhelming task. However, taking care of a few best practices can help significantly. For example:

Target to Minimize the Scope of Compliance

The best way to kickstart the journey of making your financial ecosystem compliant with PCI DSS Standards is to target gaps. Identify systems where cardholder data is stored, processed, and transmitted. Furthermore, adopt the tokenization practice to isolate sensitive data, and disguise it.

According to the quick book of the PCI Security Standards Council, segmentation of the data results in the simplification of PCI DSS implementation.

Define SAQs (Self Assessment Questionnaires)

Here are the SAQ types that can help you prepare forms to identify your business’s ability to comply with PCI DSS requirements.

| SAQ Type | Who Should Use It | Examples | Key Focus |

|---|---|---|---|

| SAQ A | Merchants outsource all payment processing to third parties. | E-commerce sites using third-party processors. | Minimal requirements as no cardholder data is stored or processed directly. |

| SAQ A-EP | E-commerce merchants outsource payments but manage their web servers. | Merchants integrating payment processors. | Securing the website and ensuring the integrity of payment pages. |

| SAQ B | Merchants are using imprint machines or standalone, non-connected POS devices. | Small brick-and-mortar stores. | Physical security and basic PCI controls. |

| SAQ B-IP | Merchants are using standalone P2PE-certified terminals connected to the Internet. | Retailers with encrypted card readers. | Internet connection security and encryption. |

| SAQ C | Merchants using payment apps connected to the Internet but isolated from other systems. | Businesses with POS software connected to gateways. | Network segmentation and security controls. |

| SAQ C-VT | Merchants manually enter transactions into virtual terminals via browsers. | Small businesses using secure portals. | Browser and workstation security. |

| SAQ D (Merchants) | Merchants store, process, or transmit cardholder data directly. | Large retailers with custom solutions. | Full PCI DSS compliance across all requirements. |

| SAQ D (Service Providers) | Service providers storing or managing cardholder data for others. | Payment processors and hosting providers. | Full PCI DSS compliance for service provider-specific requirements. |

Organize a Critical Gap Analysis

Compare your current transaction system with the latest PCI DSS compliance requirements. Ensure there are no vulnerabilities left that can later result in hefty fines, possible data breaches, or worse- both! If found, prioritize your resources to fill these gaps. If required, consider keeping regulatory bodies in the loop as well.

Take Advantage of Tokenization and Encryption

Keep your data locked, whether it’s cardholder details or payment information in transit. Use encryption software tools to lock sensitive data, limit services to users of brands that implement encryption in mobile devices, leverage security practices like Advanced Encryption Standard (AES), etc.

Organize Regular Monitoring and Testing of Systems

Implement regulator testing practices that can help you find possible vulnerabilities as soon as they occur. Integrating AI and cybersecurity for your financial products can also be a great strategy to receive quick alerts in case there are any possible attempts to steal data.

Beyond the integration of AI, financial security is also improving due to more accessible testing methods such as app testing tools.

Train Employees to Keep them Aware of PCI DSS Compliance

Organizing regular training sessions for your employees can enhance the overall strength of your PCI DSS compliance. These sessions should cover instructions related to handling payment data, following best security practices, assigning role-specific responsibilities, etc.

Adopt a Proactive Approach to Remain Compliant

Compliance is not something you can achieve at one time. It’s a regular practice that needs to remain in motion. Establish a culture that supports staying in the loop with evolving compliances. Conduct annual reviews, update systems, and stay in the loop by updating PCI DSS guidelines, such as the latest transition to PCI DSS v4.0.

Mistakes to Avoid While Implementing PCI DSS Standards

There are some common mistakes you can avoid when implementing smoother PCI DSS standards across your financial institution. Here's a short overview of these mistakes:

- Neglecting Regular Updates: Not keeping up with the latest PCI DSS versions can create a huge gap in the success of your PCI DSS compliance strategy.

- Weak Access Control: Skipping safety measures like multi-factor authentication can weaken the access control strategy making data breaches more likely.

- Bad Data Store Practices: Storing sensitive data of cardholders for no reason or without tokenization can bring unnecessary incidents and challenges.

- Ignoring Third-party Compliance: Not taking care of compliances for third-party vendors can create a gap in your compliance strategy.

- Inadequate Employee Training: Even if you have access to the right resources, bad employee training can cause more errors, exposing your fintech solution to phishing and malware attacks.

- Insufficient Monitoring and Testing Strategy: Keeping an eye on your fintech solution to identify any possible vulnerabilities is crucial for the security of your cardholder’s data.

Latest in PCI DSS Standards: v4.0 & 4.0.1

The fourth version of PCI DSS compliance guidelines brings new additions to existing guidelines. Here’s a quick go-through:

| Feature | PCI DSS v4.0 | PCI DSS v4.0.1 |

|---|---|---|

| Focus | Comprehensive updates with new security measures. | Minor revision focusing on clarity and usability. |

| Multi-factor Authentication (MFA) | Mandated for cardholder data environments, replacing password-only storage. | No new updates beyond the v4.0 requirements. |

| Tailored Security Requirements | Allows tailored requirements if companies meet better security outcomes. | No new updates beyond the v4.0 requirements. |

| Real-Time Security Analysis | Emphasizes real-time analysis for quick threat detection. | No new updates beyond the v4.0 requirements. |

| Encryption Protocols | Maintains alignment with advanced cryptographic protocols for data in transit and at rest. | No new updates beyond the v4.0 requirements. |

| Penetration Testing | Quarterly testing and detailed configuration reviews are required. | No new updates beyond the v4.0 requirements. |

| Cloud Data Security | Defines clear guidelines for securing data in cloud environments. | No new updates beyond the v4.0 requirements. |

| Third-Party Compliance | Requires companies to ensure third parties comply with PCI DSS. | No new updates beyond the v4.0 requirements. |

| Social Engineering Training | Introduces new guidelines for phishing and social engineering prevention. | No new updates beyond the v4.0 requirements. |

| Password Strategies | Brings stronger password strategies into existence. | No new updates beyond the v4.0 requirements. |

| Compliance Deadlines | Policies must be followed until March 31, 2025; PCI DSS 3.2.1 will be phased out afterward. | Clarifies that PCI DSS v4.0 expires on December 31, 2024; companies must upgrade to v4.0.1. |

| Typographical Errors | Not applicable. | Fixes typographical errors for better comprehension. |

| Supplementary Sections Adjustments | Not applicable. | Adjusts templates and definitions; sample templates moved to the PCI SSC website. |

| Expiration Dates | Not applicable. | Specifies the official expiration date for v4.0 and transition to v4.0.1. |

Wrapping Up

Let’s face it- it has become routine to know about cyberthefts, especially in the global fintech system. If these incidents are making you anxious, keeping your digital product compliant according to PCI DSS guidelines can be the solution.

Here’s a fact, though- PCI DSS standards aren’t just a collection of tick boxes. Instead, it’s a practice that will have to become regular in your business to make it more effective. However, the framework is dynamic in nature. So it’s also critical to remain in the loop with new updates coming to the guidelines.

With everything done right, it can significantly save your financial ecosystem from unauthorized theft, resulting in an established reputation, reduction of financial losses, and smooth operations.

Frequently Asked Questions

-

What does the PCI DSS regulate?

-

How to implement PCI DSS compliance in any App and Software?

-

What does PCI DSS mean in cyber security?

-

How to be PCI DSS compliance ready?

-

What are PCI DSS requirements?

-

What are some levels of the payment card industry standards?

-

What is the process of implementing PCI DSS standards?

-

Which statement properly defines PCI DSS standards?

-

What industries need to follow PCI DSS standards?

-

What happens if a company fails to comply with PCI DSS guidelines?

Sr. Content Strategist

Meet Manish Chandra Srivastava, the Strategic Content Architect & Marketing Guru who turns brands into legends. Armed with a Masters in Mass Communication (2015-17), Manish has dazzled giants like Collegedunia, Embibe, and Archies. His work is spotlighted on Hackernoon, Gamasutra, and Elearning Industry.

Beyond the writer’s block, Manish is often found distracted by movies, video games, AI, and other such nerdy stuff. But the point remains, If you need your brand to shine, Manish is who you need.